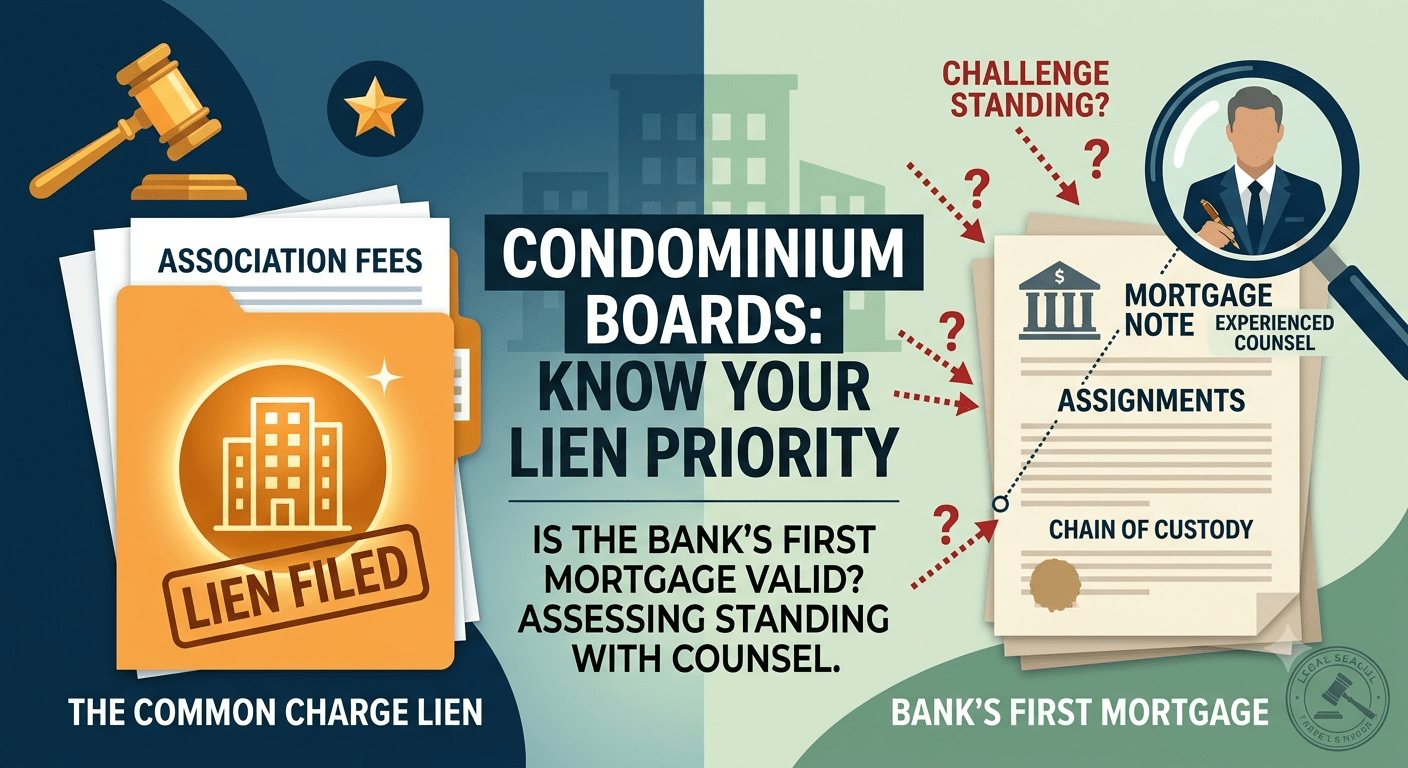

When a condominium unit owner defaults on their monthly common charges, the board’s primary tool for recovery is filing and foreclosing on a common charge lien. However, condominium boards routinely run into a frustrating roadblock: the priority of the first mortgage. Under standard real estate law, a bank’s first mortgage typically takes priority over a condo’s common charge lien. Because bank foreclosures can end with the bank taking back the property at auction—or with no surplus funds left over after the bank’s debt is paid—condominiums don’t get paid and have to resort to other tools to recover against the foreclosed unit owner.

But it doesn’t always have to be a dead end.

While challenging a bank’s mortgage priority is not a routine or mandatory requirement for every foreclosure, sophisticated condominium boards should be aware that it is a viable legal possibility. By understanding the mechanics of bank foreclosures and engaging experienced legal counsel, boards can evaluate whether a bank’s claim to primary priority is actually valid, or if the condo’s common charge lien has a chance to step into the winner’s circle.

The Power of Priority: A Possibility Worth Investigating

In a typical foreclosure scenario, a bank’s first mortgage must be satisfied before any junior liens receive a dime. If a unit goes to a foreclosure auction and the sale price doesn’t exceed the bank’s loan amount, there is no “surplus,” and the condominium board doesn’t get back from the foreclosure. There are other ways to get paid but the foreclosed unit is no longer available to secure the unit owner’s debt to the condominium.

However, a mortgage is only enforceable if the entity bringing the foreclosure action has the legal right to do so. In real estate litigation, this is known as standing. To have standing in a mortgage foreclosure action, a bank must prove that it was the actual holder or assignee of the underlying promissory note at the exact moment the lawsuit was commenced.

Because banks frequently bundle, sell, and transfer mortgages through complex securitization pools, critical paperwork—like the original note, assignments, and powers of attorney—is sometimes misplaced or improperly executed. If a bank files a foreclosure action but cannot prove it legally held the note on day one, its foreclosure can fail. For a condominium board, if a bank cannot establish standing, its priority claim is compromised, opening up the rare but powerful possibility that the condo’s common charge lien could move into the primary position to collect what is owed.

A Lesson from the Courts: U.S. Bank N.A. v. Speller

A decision from the New York Appellate Division, U.S. Bank N.A. v. Speller, perfectly illustrates just how heavily litigated and technically demanding the issue of a bank’s standing can be.

In the Speller case, U.S. Bank commenced a mortgage foreclosure action against individual unit owners. The defendants raised the affirmative defense that the bank suffered from a lack of standing. The trial court initially agreed with the defendants, taking the drastic step of dismissing the bank’s complaint entirely.

While U.S. Bank ultimately won on appeal by bringing in meticulous testimony from a third-party note custodian and producing pristine business records to prove they physically possessed the original note at commencement, the case highlights a critical lesson: a bank’s standing is not a foregone conclusion. The bank had to endure a full trial and a subsequent appellate battle just to prove it had the right to foreclose.

The Crucial Role of Experienced Counsel

Navigating the intersection of condominium law and mortgage foreclosure litigation is highly technical. It is not something a board should look into without guidance, nor is it a strategy to deploy blindly in every case. Instead, this is a tool for your legal arsenal to be evaluated with experienced counsel.

An experienced condominium attorney can help your board by:

Evaluating the Risks and Rewards: Reviewing the bank’s initial filings to look for glaring chain-of-custody gaps or missing note endorsements.

Determining Feasibility: Assessing whether a bank’s potential standing issue is weak enough to warrant a formal legal challenge, ensuring the board does not waste community funds on fruitless litigation.

Protecting the Association’s Interesets: Keeping a watchful eye on the bank’s foreclosure timeline and ensuring the condo is positioned to capture any unexpected surplus if the property does sell.

When a bank takes back a property because there are no external buyers at an auction, the condominium is usually left holding the bag for months or years of unpaid common charges. While you cannot challenge every first mortgage, simply being aware that a bank’s priority depends entirely on its legal standing changes the dynamic. By working closely with experienced counsel to spot these unique opportunities, condominium boards can aggressively protect their communities’ financial health and ensure they aren’t leaving money on the table.